- Why private business acquisitions can help generate consistent investment income outside the stock market.

- How self-directed retirement capital may be used to participate in carefully structured private investments.

- Why more investors are seeking alternatives to traditional markets — and how to capitalize on that shift.

- Investor information is kept confidential

- Speak directly with our team

- No obligation

Maybe you missed Bitcoin. Maybe you missed NVIDIA at $21.

Maybe you even remember $35/ounce gold. This opportunity is worth your attention.

While crypto skyrockets and blue chips get bid past fair value, small and mid-sized businesses are still trading at reasonable multiples. Why? Because the people who want to own them can’t get SBA financing. That mismatch means: sellers waiting over a year just to swallow lowball offers, brokers starving for commissions, and high-quality businesses with real estate selling for only 2–2.5× EBITDA (DSCR > 2.0x). In fact, the last few we reviewed included property and still came in at just 2.2× earnings.

That’s not theory — that’s market inefficiency you can step into.

We’re currently aligning capital for this round with the goal of completing fundraising by the end of the third quarter of 2026. Investor funds are contractually scheduled for deployment within six months, unless otherwise agreed in writing. Since this is one of our flagship ventures, investment capital required is intentionally limited.

10%: $110,000

10%: $161,051

10%: $259,374

If you’ve been looking for an opportunity to diversify into private business acquisitions, we encourage you to review the materials carefully. Questions? Give us a call — we’ll answer everything.

Accredited investor intake for this round closes September 30, 2026. Contact us to reserve your position for contractually scheduled deployment within six months, unless otherwise agreed in writing.

This letter is falling out of the investor kit for a reason: it’s your signal that now is the time to raise your hand. If you’re serious, call directly at (833) 319-3160 (press 0 anytime to reach me directly) or reply to this letter before the deadline.

- 6.5% compounded pre-deployment return

- Contractual deployment within six months, unless otherwise agreed in writing

- Independent third-party legal, financial, and operational due diligence before deployment

- 16% contractual post-deployment return with quarterly payments unless compounding is elected

- Seven-calendar-day buyer’s remorse / cooling-off period after signing

- Reporting and audit rights built into the agreement

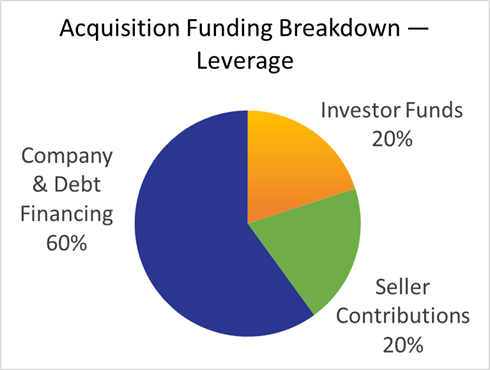

How can we promise 16% returns? Because we leverage investor funds while also utilizing traditional institutional financing. That means bigger deals, stronger cash flow, and more money in your bank account.

In plain English: the goal is not to limp into a tiny all-cash deal. The goal is to control a larger productive business with disciplined leverage, third-party due diligence, and a structure built to throw off more income.

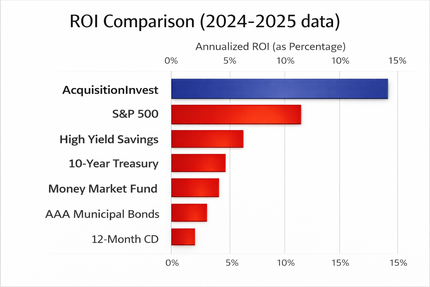

Blue chips are not magical. This chart exists to break the lazy assumption that public-market names are automatically safer just because they are familiar. Serious investors look at actual risk, actual default behavior, and actual deal structure.

Public markets often price stories. Private business acquisitions can still be structured around disciplined valuations, real cash flow, and operating companies with actual customers, staff, and recurring demand.

- Cash flow driven by operations instead of market sentiment

- Disciplined acquisition structures instead of chasing inflated public multiples

- Real businesses serving real customers in the real economy

Eligible investors may participate through a self-directed IRA, custodian, trust, or other fiduciary retirement structure, subject to required documentation.

That means retirement capital may be used to pursue structured private investment returns outside the traditional public-market box.

A $100,000 investment compounding at 16% grows about $181,770 more over 10 years than the same $100,000 compounding at 10%.

Why does this matter? Because a few extra points of annual return can turn into a massive gap over time. That is why serious investors request the kit instead of shrugging and settling for average.

AcquisitionInvest.com

AcquisitionInvest.com

FAQ

You Have Questions.

They Deserve Real Answers.

Here is the uncomfortable truth about the stock market that no one on television wants to say plainly: when you buy shares in a public company trading at twenty-five times earnings, you are not buying a business. You are buying a story about a business — a story that depends entirely on the next buyer believing it more fervently than you do.

AcquisitionInvest does something categorically different. We acquire real operating businesses — companies with employees on payroll, customers who pay invoices, and recurring revenue that does not care what the Dow did this morning.

The return you receive comes from the distributable cash flow those companies actually produce — not from multiple expansion or speculative narrative. That is a fundamentally different proposition.

This is exactly the question a rigorous mind asks first. Good.

The answer comes down to access, not quality. Most people who would gladly purchase these businesses cannot access SBA financing or acquisition capital. Large institutional funds ignore them because they are too small. Individual buyers lack the systems and capital to act decisively.

On the seller's side: baby boomer founders who spent three decades building something valuable, who now want certainty and a clean exit. They are not trying to extract the last theoretical dollar. They want the transaction done correctly.

High-quality businesses with real estate and recurring revenue can still sell at 2.0–2.5× EBITDA with debt service coverage above 2.0×. That is not a market failure. That is a market inefficiency disciplined buyers have been profiting from quietly for decades.

Capital is held in escrow or custody prior to deployment — it is not co-mingled with operating funds, and personal use is expressly prohibited by the agreement. During the pre-deployment period, the structure provides for a custodial interim return, so your capital is not simply sitting idle while due diligence proceeds.

More importantly: we have a fiduciary duty to avoid reckless deployment. If the right acquisition is not available, we wait. Undisciplined speed destroys more capital than patient discipline ever will.

Absolutely not. There is an enormous difference between owning cash flow and owning a job. Many small business investments fail for one precise reason: the buyer discovers too late that he has purchased employment disguised as ownership.

Under the agreement, your rights are strictly economic. AcquisitionInvest maintains full responsibility for sourcing, due diligence, acquisition execution, management, legal oversight, and day-to-day operations. Those roles do not cross.

You are a passive capital partner. You did not spend decades building your savings so that retirement could hand you a second career in a business you never planned to enter.

Most people are never told this: a retirement account is a container, not a worldview. The account does not dictate what it holds — that depends entirely on how it is structured.

Through a Self-Directed IRA, eligible investors can legally allocate retirement capital into private business acquisitions while maintaining the tax-deferred character of the account. Because operations are fully managed by AcquisitionInvest, passive investors avoid UBIT and UDFI exposure.

Consult with a qualified tax or legal advisor before making any SDIRA allocation decision. That is not boilerplate — it is genuinely important.

Acquisition risk is real. Sellers present numbers optimistically. Operational weaknesses can remain hidden until a deal closes. This is why we require independent third-party due diligence before any capital is deployed.

Leverage risk is real. We address it by targeting a Debt-Service-Coverage Ratio of at least 2.0× — the business earns roughly twice what is needed to service debt. That cushion is the margin between a difficult quarter and a financial crisis.

Cooling-off protection exists. The agreement provides a seven-calendar-day buyer’s remorse / rescission period after signing, subject to the contract terms.

Liquidity risk is real. This is not a stock you can sell in thirty seconds. The agreement provides a two-year termination right after deployment — more investor-friendly than traditional private equity lockups — but your capital will not be instantly accessible.

The 16% annual post-deployment return is contractually guaranteed under the written investment agreement, subject to the agreement terms. This is not a stock-market projection, speculative appreciation claim, or marketing target. The structure is built around acquisition cash flow, disciplined underwriting, and contractual investor payment obligations.

Under the agreement, you may terminate after two years from deployment by giving notice and may request return of principal — including reinvested amounts where applicable — subject to the agreement's terms.

This does not make it a liquid instrument resembling the stock market. But it means you are not signing a decade of your financial life away. Life does not conform perfectly to investment timetables, especially for retirees. The structure acknowledges that reality.

Capital exists to serve life — not the other way around.

Trent Tompkins — Founder, Finance, Due Diligence, and Acquisitions. Software developer and business builder who has already owned and exited a SaaS business that sold for $750,000. Disciplined acquisitions require systems thinking and financial analysis — the kind built from having already done the hard work of building something to exit.

Corey Rodriguez — Chief Strategy Officer, Customer Relations. Background in account management, sales, and negotiation. Deals collapse because of relationship failures far more often than financial ones. His role ensures inquiries are handled with the clarity serious capital deserves.

You are engaging directly with two people who are accountable by name, reachable by phone, and whose success depends on disciplined execution — not a single transaction and a disappearance.

You receive monthly operating summaries during the first twelve months after acquisition, quarterly financial statements thereafter, and immediate notice of any material adverse events. You also hold full audit rights — the ability to review financial records at any time.

This is not a courtesy. It is a contractual obligation. Transparency is the precondition of trust. A serious investment does not tell you to trust it — it gives you the tools to verify it.

The process is structured. Accredited investors may be asked to complete an Accredited Investor Affidavit, an AML / KYC questionnaire, an OFAC / sanctions representation, a source-of-funds certification, and a tax reporting cover sheet, depending on how they participate.

That paperwork is not there to waste your time. It is there to keep the offering compliant, document the source of capital properly, and make sure everyone is operating inside a real process rather than a vague promise.

Step one: Request the full Investor Kit. Review the acquisition strategy, financial illustrations, and governing documents carefully.

Step two: Confirm your accredited investor status. This offering is structured under Rule 506(b) of Regulation D.

Step three: Schedule a direct conversation. Ask every question that matters. A serious structure welcomes scrutiny.

Step four: Review the agreement with independent legal or tax counsel.

Step five: Make your allocation decision and elect your preference — cash distributions or compounding reinvestment.

Accredited investor intake for this round closes September 30, 2026. Once fully subscribed, additional investors wait for the next opportunity.

Call or text (833) 319-3160 or email invest@acquisitioninvest.com.

This offering is available to accredited investors only. You can review and download the affidavit here: Accredited Investor Affidavit (PDF).

Under SEC Rule 501(a), an accredited investor includes, among others: certain regulated institutions and fiduciary plans; private business development companies; certain 501(c)(3) organizations, corporations, partnerships, LLCs, Massachusetts or similar business trusts with total assets over $5,000,000 that were not formed just to buy the offered securities; directors, executive officers, or general partners of the issuer or its general partner; natural persons whose individual or joint net worth exceeds $1,000,000 excluding the primary residence; natural persons whose individual income exceeded $200,000 in each of the two most recent years, or joint income with spouse or spousal equivalent exceeded $300,000 in each of those years, and who reasonably expect the same income level in the current year; certain trusts with total assets over $5,000,000 whose purchase is directed by a sophisticated person; entities in which all equity owners are accredited investors; certain other entities owning investments in excess of $5,000,000; natural persons holding in good standing qualifying professional certifications, designations, or credentials recognized by the SEC; knowledgeable employees of certain private funds; qualifying family offices with over $5,000,000 under management; and certain family clients of qualifying family offices.

For most U.S. investors, the practical question is simple: do you meet the net-worth or income standard, or do you qualify under another SEC category such as recognized professional credentials or a qualifying entity structure?

For U.S. individuals, the answer is usually simple: you only need to complete an IRS Form W-9 (PDF).

The other two forms are included for completeness and are generally for foreign investors or foreign entities, which most investors on this page will not need: IRS Form W-8BEN (foreign individuals) and IRS Form W-8BEN-E (foreign entities).

If you are investing as a normal U.S. individual, start with the W-9. If you are using a more unusual structure or are unsure which form applies, ask us and we will point you in the right direction.

Still Have Questions? Good.

Serious capital deserves direct answers. Call us, ask everything, and decide from clarity — not momentum.

(833) 319-3160 — Call or Text FreePhotos

Photo gallery coming soon.

Team

Real Operators.

Real Accountability.

Most investment firms hide behind logos and polished brochures. We put our names on it — because when your capital is on the line, you deserve to know exactly who is answering the phone.

Pittsburgh Office

Pittsburgh Office

Pittsburgh, PA

Pittsburgh, PA

Trent Tompkins

Founder — Finance, Due Diligence & Acquisitions

There is a particular kind of person who builds something from nothing, watches it work, sells it — and then asks himself: what’s next, and how do I do it bigger? That is Trent Tompkins.

Trent founded AcquisitionInvest LLC after a career as a software developer and entrepreneur that culminated in the successful sale of a SaaS business for $750,000. That exit was not an accident. It was the result of systems thinking, financial discipline, and the willingness to do the unglamorous work of building something durable — not just impressive.

“Anyone can talk about buying businesses. Very few people understand how to underwrite one, structure the capital correctly, and operate it so it actually pays you.”

As the officer responsible for Finance, Due Diligence, and Acquisitions, Trent owns the most consequential part of the process: deciding which businesses deserve your capital, and which ones do not. His background in software — a field built entirely on logic, systems, and the brutal honesty of things that either work or do not — translates directly into acquisition discipline. He is not interested in stories. He is interested in numbers that survive contact with reality.

He is also the person who will tell you no. Not because he is cautious for the sake of caution, but because protecting investor capital is not a courtesy — it is the job. Trent is directly reachable. No gatekeepers. No voicemail maze.

Corey Rodriguez

Chief Strategy Officer — Investor & Seller Relations

Every deal lives or dies in the conversation. Not the spreadsheet — the conversation. The moment where a seller decides whether to trust you. The moment where an investor decides whether the people behind the opportunity are serious or merely well-dressed. That moment belongs to Corey Rodriguez.

Corey brings a career forged in customer relationships, account management, sales, and negotiation — the real-world disciplines that determine whether opportunities close or collapse. He has spent years learning how people make decisions, what they are actually afraid of, and how to deliver clarity when the stakes are real.

“Most investors don’t need more information. They need a straight answer from someone who’s accountable for what happens next.”

As Chief Strategy Officer, Corey is responsible for investor communication, seller relationships, and making sure serious inquiries are handled with precision — not with scripted enthusiasm or hollow reassurance. When you call this company with a real question, Corey is the kind of person who gives you a real answer.

He also serves as the bridge between the financial architecture Trent builds and the human beings who need to understand it. That is not a soft skill — in private placements, the ability to communicate structure clearly and earn trust honestly is what separates firms that execute from firms that only pitch. Corey handles investor inquiries directly. If you have questions, reach out.

Ready to Have a Real Conversation?

No pitch decks. No hard sell. Just direct answers from the people responsible for putting your capital to work. If this opportunity fits your situation, we will tell you. If it does not, we will tell you that too.

250 Mt. Lebanon Blvd, STE 210

Pittsburgh, PA 15234